Is Transferring Crypto a Taxable Event?

According to the Internal Revenue Service (IRS), most cryptocurrencies are convertible virtual currencies. They may, therefore, be used in place of actual money and serve as a medium of exchange, a store of value, a unit of account, and a unit of worth.

Additionally, it implies that any earnings or revenue derived from your cryptocurrencies are taxed. However, there is a lot to understand about how cryptocurrency is taxed since, depending on the circumstances, you may or may not owe taxes. Knowing when you will be taxed is crucial if you own or use cryptocurrencies so that you are not taken aback when the IRS comes to collect it.

If you’re one of the more than 10% of Americans who traded cryptocurrencies in the last year, you undoubtedly have questions about how your transactions and other cryptocurrency activities will affect your taxes.

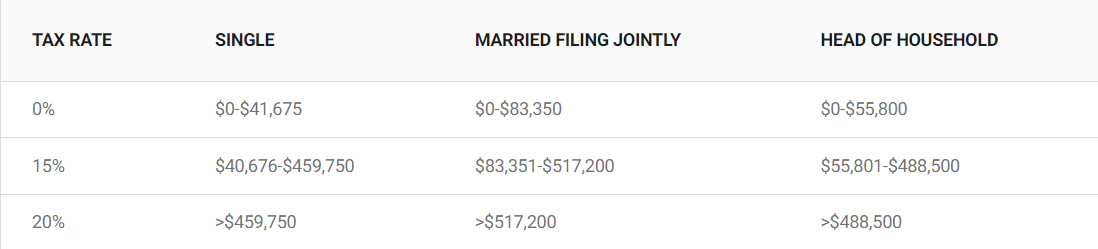

Crypto Tax Rates 2023

For 2022, the IRS changed the tax brackets to reflect inflation. Here are the long-term cryptocurrency tax rates that will apply when you file your 2022 tax return.

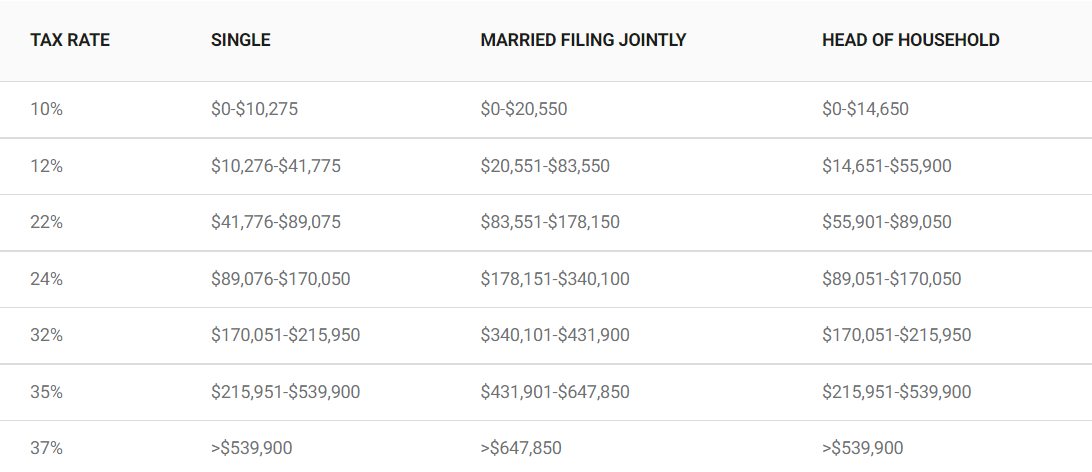

As previously mentioned, the IRS taxes short-term cryptocurrency profits as regular income. Here are the tax rates for 2022 that will be applied to cryptocurrency earnings held for 365 days or fewer.

What is Capital Gains Tax in Crypto?

Some investors purchase cryptocurrencies, wait for the price to rise, and then exit their investments. Other investors sell off certain cryptocurrencies to diversify their portfolios and lower risk.

If your selling price exceeds your cost basis, these transactions may result in capital gains taxes. The cost basis is the amount you forked over to buy cryptocurrency.

The IRS will tax your profits depending on your income level and the length of time you held the post. Before selling, keep your cryptocurrency for at least a year to get a better tax rate.

Some investors sell cryptocurrency at a loss to pay less taxes.

The wash sale rule does not apply to cryptocurrency since the IRS views it as a property rather than a security. You may sell your cryptocurrency at a significant loss and buy it again right away.

Your records will still reflect the net loss, which will help you pay less in taxes. For stocks, the wash sale rule is applicable. If you want your net loss to stand for taxation reasons, you cannot repurchase the identical stock for 30 days.

What is Income Tax in Crypto?

Some businesses use Bitcoin to pay their employees. Additionally, you could get paid in cryptocurrency for recommending specific goods or taking part in activities that do. These payouts are regarded as part of your income.

You must file a tax return if you receive $500 in cryptocurrency in exchange for services. No matter how much the crypto’s value rises or falls over time, you will still have to pay income taxes on that $500. Some people relocate to states with no income taxes to escape this debt.

What are Taxable as Capital Gain Cryptocurrency Events?

Cryptocurrencies and assets both have uses. You can acquire, keep, and ultimately sell this asset. A merchant may accept it in return for products and services, or you may engage in day trading in cryptocurrencies.

Understanding how cryptocurrency taxes operate might help you preserve your earnings and save money. We will discuss several frequent cryptocurrency-related taxable occurrences and money-saving strategies.

Cashing Out Crypto for Fiat

Capital gains are possible when you cash out your cryptocurrency. Securing a profit increases your financial situation, but it is also a taxable event.

If your business generates a net profit, the IRS will examine your transactions and tax you. You will have capital gains if you sell your property for more than your cost basis.

Any losses can be used to reduce your tax liability and write them off.

Converting a Cryptocurrency

When it comes to taxes, the IRS views cryptocurrency as property. Although it’s a resource that some individuals utilize as money, the Internal Revenue Service’s perspective is most important in terms of taxes. Crypto-taxed events also include the conversion of cryptocurrencies.

Even if you exchange Bitcoin for Ethereum, you will still need to disclose the transaction and pay any applicable capital gains taxes.

Purchasing Goods and Services with Crypto

Several businesses already accept crypto as a form of payment, and some proponents believe it will eventually displace traditional money.

Despite the fact that the decentralized aspect draws many investors, using it as a medium of exchange will result in capital gains.

The tax consequences of using crypto as a means of trade are the same as those of selling crypto for fiat money.

You are spending crypto for an item or service rather than fiat cash.

Capital gains rates are regulated by the IRS for both short- and long-term investments. You would receive more advantageous tax treatment if you keep the asset for more than a year.

What are Taxable as Income Tax Cryptocurrency Events

Receiving Crypto as Payment

Crypto payments are recognized as income when you receive them, and the revenue must be reported to the IRS.

For instance, if you get crypto worth $500 as payment, $500 will be subject to tax. By retaining the cryptocurrency, you cannot postpone this tax.

Mining or Staking Crypto

Both of these events’ proceeds are classified as regular income. Based on the value of the cryptocurrency at the time of the transaction, taxes will need to be paid.

The process of validating and adding Bitcoin transactions to a blockchain is known as crypto mining. Miners get paid in cryptocurrencies in return for their labor.

Receiving Crypto in Play-to-earn Games

Play-to-earn gaming rewards in the form of cryptocurrency are considered regular revenue. Your tax bracket may increase if you earn enough cryptocurrency.

As you plan your spending and save money, you should think about how cryptocurrency may affect your taxes.

Earning other income

Holding some cryptocurrencies can result in a return for you. This qualifies as taxable income.

The IRS does not treat this like interest you might receive from a bank, despite the fact that it is commonly referred to as interest.

Receiving an Airdrop

Any airdrops must be reported as regular revenue. Your tax rate will be determined by your income bracket.

The cryptocurrency’s fair market value as of the receipt must be reported. You must still record any airdrops you receive to the IRS, no matter how tiny.

Participating in a Hard Fork

A hard fork is a significant modification to the protocol of a blockchain network that renders invalid previously validated transaction history blocks or the opposite. A cryptocurrency will frequently engage in a hard fork because it wants to establish a new regulation for the blockchain.

While the old chain lacks the new rule, the new, updated blockchain does. As a result of the hard fork, many users of the old blockchain soon come to the realization that their old version of the blockchain is obsolete or useless, requiring them to update to the most recent version of the blockchain protocol.

A hard fork does not always result in the taxpayer receiving new bitcoin, and as a result, it does not always cause a taxable event. If a hard fork takes place and is followed by an airdrop where you receive fresh virtual money, on the other hand, this produces regular revenue.

Whether or whether you obtain a 1099 form disclosing the transaction, this qualifies as taxable income on your tax return and must be reported to the IRS.

What are Non-Taxable Cryptocurrency Events?

Capital gains taxes will apply if you sell Bitcoin or use it as money. Sometimes, you can avoid depreciation by selling and paying taxes. The cryptocurrency market is difficult to anticipate, but cutting your taxes is simpler. These techniques can help you reduce your cryptocurrency taxes.

Purchase Crypto With USD/Fiat

When you use another coin to buy a crypto, the previous holding will have capital gains. Purchasing crypto with fiat money is not taxed. Therefore, holding onto your cryptocurrency is preferable to selling it in order to acquire another one. If you wish to diversify, you can invest money from your next paychecks in your next crypto.

Buy Crypto in an IRA

The Internal Revenue Service (IRS) does not recognize any particular Individual Retirement Account (IRA) created for crypto. As a result, when you hear the terms “cryptocurrency IRA” or “Bitcoin IRA,” they refer to an IRA that has digital currencies as part of its assets.

For people saving for retirement and investing, IRAs provide tax benefits. With a Roth IRA, you can invest and never pay capital gains tax. With just a 1% transaction fee and no additional fees, iTrustCapital enables you to build a cryptocurrency IRA account.

Hold Crypto

If you keep your cryptocurrency, you’ll never have to pay taxes on it. You can wait to sell until you are ready and let the capital gains accumulate. You can avoid paying capital gains taxes by moving to Puerto Rico or holding off on selling your cryptocurrency until after retirement.

Cryptocurrency purchases and ownership alone are not taxed. When you sell something and the earnings are “realized,” the tax is frequently paid later.

Transfer Between Your Own Wallets and Exchanges

Since you still own the cryptocurrency after the transfer, moving it from one wallet or exchange to another is not a taxable event. Some investors inadvertently sell cryptocurrency for cash, transfer the money to a different site, and then buy cryptocurrency again. Transferring money between exchanges and wallets is simpler and won’t affect your taxes.

Give or Receive Crypto as Gifts

Most cryptocurrency gifts are tax-free. The IRS has set restrictions on how much you may gift each year ($15,000) and overall ($11.7 million) before it triggers a tax obligation. The receiver should be informed of the purchase date and cost basis. If the receiver sells the cryptocurrency you send them, they will want this information for tax purposes. Without paying taxes, you can give up to $15,000 to each recipient each year (and higher amounts to spouses).

Donate Crypto to a Qualified Nonprofit

You can be eligible for a charitable deduction if you donate cryptocurrency directly to a nonprofit like GiveCrypto.org, without worrying about taxes.

Cryptocurrency Tax Reporting

You’ll need to be slightly more prepared throughout the year than someone who doesn’t have assets if you want to submit your taxes accurately. For instance, you must make sure that you keep a record of each cryptocurrency transaction, including the amount you spent and the currency’s market value at the moment you used it.

How much do you owe in crypto taxes?

It appears that part of your cryptocurrency activity is taxable. By figuring out your income, profits, and losses, you can determine how much tax you will owe. The amount you spend or swap, your income level and tax bracket, and how long you’ve owned the cryptocurrency you spent will all affect how much tax you owe on it.

Calculating Cryptocurrency Income

If you pay taxes in the United States, you’re undoubtedly accustomed to seeing deductions for federal and state income taxes on your pay stubs. The income taxes that apply to other forms of income, such as mining, staking, and rewards, also apply to cryptocurrency earnings, albeit they are frequently not withheld or deducted.

You’ll typically owe what your tax bracket-appropriate income tax rate is when you submit your earnings.

Calculating Capital Gains and Losses

You must first know how much cryptocurrency you had before you started in order to determine how much you made or lost. The term “cost basis” refers to this.

Your cost basis for purchasing cryptocurrencies is often established by the price you pay. The fair market value at the time you obtained the cryptocurrency, however, governs your cost basis whether you acquired it through mining or staking.

The basis the person who transferred the cryptocurrency to you possessed, as well as the fair market value at the time of receipt, will determine your cost basis for any gifts of cryptocurrency.

What is long-term Capital Gain Tax?

The transaction will be subject to long-term capital gain tax rates if you retain your cryptocurrency asset for more than a year before exchanging it for another, selling it for fiat money, or using it to make a purchase.

The tax rate on long-term capital gains is 0%, 15%, or 20%, depending on the taxpayer’s annual income, which is much lower than the rate on ordinary income. For instance, you would have a long-term capital gain of $15,000 if you purchased.5 BTC for $20,000 and held onto it for two years before selling it for four ETH worth $35,000 instead.

If you only have a salary of $100,000 during the year of the exchange, you would be subject to a capital gains tax of 15% and owe $2,250 in cryptocurrencies.

What is short-term Capital Gain Income tax?

You will owe short-term capital gains tax on any earnings you make if you sell your crypto asset within a year of buying it unless you give it away or donate it.

Your standard crypto income tax implications apply to short-term capital gains, just like it does to any revenue from mining, staking, or airdrops.

Your income tax rate will range from 10% to 37% based on your annual adjusted gross income.

Let’s say you were able to mine 1 BTC successfully while it was worth $10,000. You sell it for $15,000 in fiat cash six months later. You only have a $100,000 salary as additional money for the entire year.

As a single filer, your marginal income tax rate is 24%. If mining was your hobby, you would report $5,000 in short-term capital gains and $10,000 in mining revenue on your IRS tax forms. You would owe $3,600 in Bitcoin taxes for the whole tax year.

Understanding Capital Losses

When you sell an asset for less than what you purchased for it, you’ve experienced a capital loss. However, you may use losses to your advantage. You can utilize losses to match dollar-for-dollar any other capital gains (including those from non-crypto assets, like stocks), possibly lowering your overall tax burden.

Conclusion

Using crypto could be quite difficult since you have to keep track of your cost basis, note your effective realized price, and then you could have to pay taxes even without an official Form 1099 statement.

Additionally, the IRS is increasing enforcement and oversight of possible tax avoidance by closely monitoring who is exchanging crypto. These elements make cryptocurrencies more challenging to use and are likely to impede their further adoption.